India just posted a record export year, yet it still ships in billions of dollars worth of products it could make at home. Hidden inside the country's import-export ledgers is a map of exactly where domestic demand outstrips domestic supply. For an entrepreneur or manufacturer, that gap is not an economic curiosity. It is a list of fundable, policy-backed opportunities waiting for someone to act.

This article distills India's trade intelligence into the patterns that matter: where the country adds value, where it depends dangerously on imports, and where smart founders can build the next import-substitution success story. A recycled-plastic or agri-waste pallet venture in Chhattisgarh is one concrete, fundable example of exactly this kind of import-substitution play. The numbers below come straight from official trade data, and the most striking ones repeat a single theme. India frequently has the demand and the workforce; what it lacks is the upstream capability and the technology to capture the value at home.

The Big Picture: A Record Year With a Catch

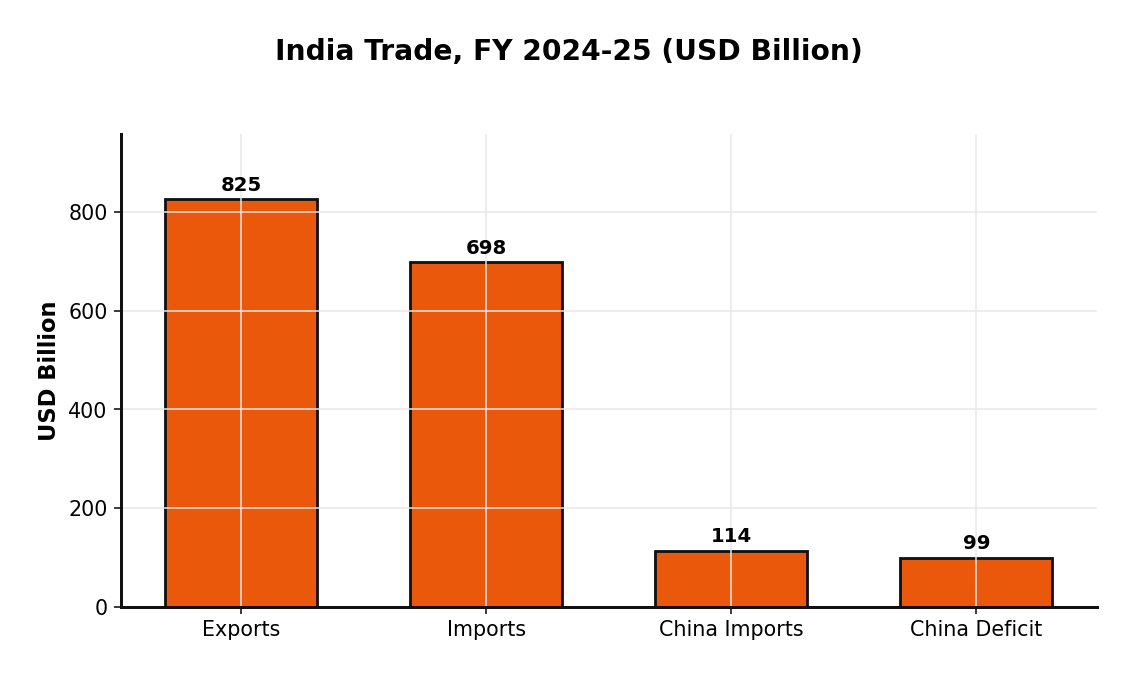

In FY 2024-25, India's trade hit new highs, but the balance tells a more nuanced story.

- Exports: $824.9 billion, a record high

- Imports: $697.75 billion

- China deficit alone: roughly $99 billion, on $113.5 billion of imports

The headline export number is genuinely impressive. The catch is what sits inside that import pile: electronics, chemicals, pharmaceutical ingredients, and solar equipment, much of it from a single trading partner. That concentration is a risk for the economy and an opening for builders. Every line item India is forced to import is a market with guaranteed, pre-existing demand.

The Value-Add Arbitrage: India Already Does This

The most reassuring evidence that import-substitution works is that India already runs several of the world's best value-add operations. The model is simple: import a raw material cheaply, process it with skilled labour and technology, then export the finished product at a multiple of the input cost.

- Diamonds: India polishes roughly 90% of the world's diamonds in Surat. Rough stones come in at around $100-200 per carat; polished stones go out at $500-2,000 per carat, a value-add of 5 to 10 times, supporting over $20 billion in annual polished exports.

- Cashews: India is the largest cashew processor on earth, importing $1.36 billion of raw nuts (1.19 million tonnes, mostly from Africa) and exporting $339 million of processed kernels, while feeding the world's largest domestic market.

- Pigeon peas (toor dal): India imports roughly 2 lakh tonnes, polishes them domestically, and re-exports to the very countries that supplied them.

The lesson is repeatable. Wherever the same raw material can be processed into a higher-value form, there is an arbitrage. The differentiator is rarely the raw material itself; it is the processing technology, logistics, and quality control around it.

The same pattern runs through India's metals trade, where the country simultaneously imports and exports closely related products:

- Steel: India imports high-grade specialty and stainless steel while exporting standard carbon steel and long products, and is a heavy importer of steel scrap for recycling. The gap, specialty steel production and recycling technology, is the opportunity.

- Copper and aluminium: The model is import the scrap, refine or process it, and export refined or semi-finished metal. Anyone who improves recovery yields or processing efficiency captures margin on every tonne.

- Textiles and leather: India imports synthetic fibers, high-end fabrics, raw hides, and processing chemicals, then exports garments, home textiles, and finished leather goods. Technical textiles for defense and industrial use remain a largely imported, high-value gap.

These same-product import-and-export loops are a tell. They prove the domestic processing ecosystem exists; it just has not yet climbed to the highest-value or most specialised rungs of the ladder.

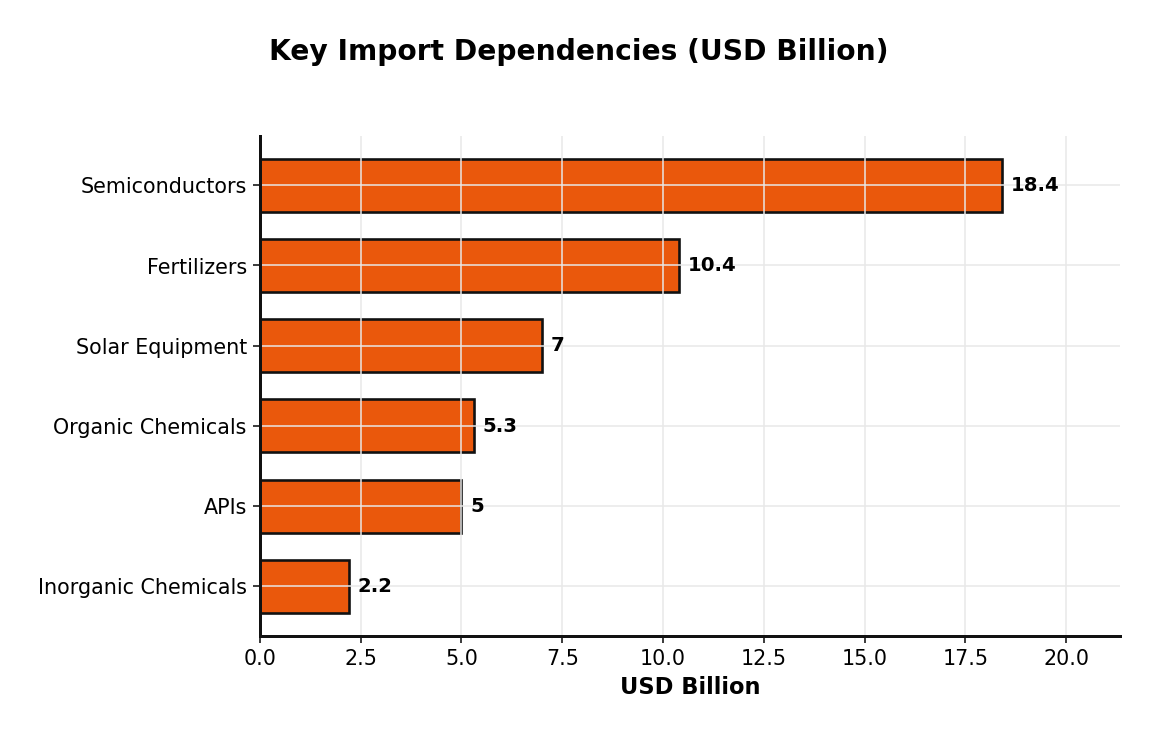

The Import Dependencies Worth Building Around

The richest opportunities sit where India has strong demand but weak upstream capability. These are not speculative markets. The demand already exists and is being met by imports today.

Semiconductors and electronics. India imported roughly $18.4 billion of semiconductors and is the world's 5th largest importer. The government is investing $18.2 billion across 10 fab projects, with the market projected to reach $110 billion by 2030. The near-term openings are in ATMP (assembly, testing, marking, and packaging), chip design services, and specialised equipment, not just the headline-grabbing fabs.

Active Pharmaceutical Ingredients (APIs). The "Pharmacy of the World" depends on China for 68-72% of its APIs, importing over $5 billion annually. Some essential drugs are 80-100% China-dependent, and bulk drug imports have grown 64% in five years. A Production-Linked Incentive (PLI) scheme now covers 53 critical APIs, making fermentation-based production and continuous-flow chemistry timely bets.

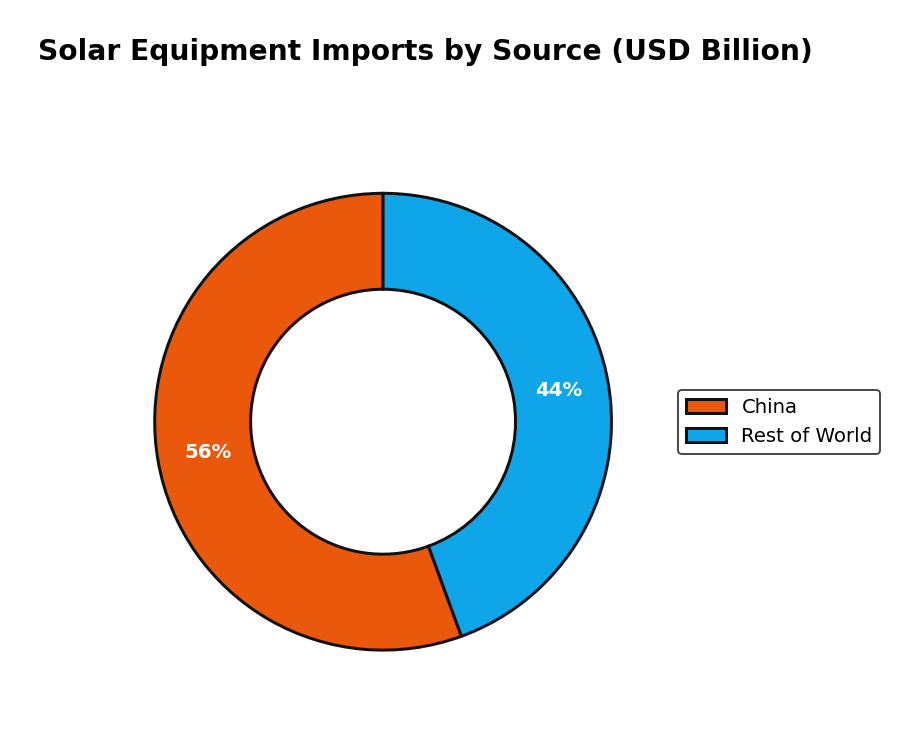

Solar cells and modules. India imported about $7 billion of solar equipment, with $3.89 billion (62.6%) from China alone, and cell imports from China grew 141% year over year.

What makes solar uniquely attractive is policy certainty: from June 2026, all clean-energy projects must use locally made solar cells. That single rule converts an import line into a guaranteed domestic market, rewarding anyone building polysilicon, wafer, or cell-manufacturing capability.

Medical devices. A market of $11-12 billion that is 70% imported, with a stated target of a $50 billion market and just 35% import reliance by 2030. Even domestic producers source 44% of their inputs abroad, leaving room in component manufacturing, calibration, and refurbishment.

Fertilizers. India imports 50-60% of its DAP and 100% of its Muriate of Potash (MOP). Alternative potash sources, nano-fertilizers, and slow-release formulations that cut the quantity needed are all viable angles.

Edible oils. India is the world's largest edible-oil importer, spending an estimated $15-20 billion a year on palm, soybean, and sunflower oil. Expanding oilseed-crushing capacity and extraction technology for domestic oilseeds directly attacks that bill.

Chemicals. The government has flagged 100 products for local manufacturing, with organic chemical imports at $5.3 billion and inorganic at $2.2 billion for a recent four-month window, covering staples like phenol, acetone, methanol, and caustic soda.

Proof That Policy Creates Markets

Skeptics will ask whether import substitution actually works in India. Two recent case studies say yes, decisively.

Mobile phones are the flagship. Under the PLI scheme, production roughly doubled in four years and exports rose 8x, with smartphone exports hitting Rs 1 trillion in just five months of FY26. Across PLI schemes, India attracted Rs 1.76 lakh crore in investment and created around 12 lakh jobs.

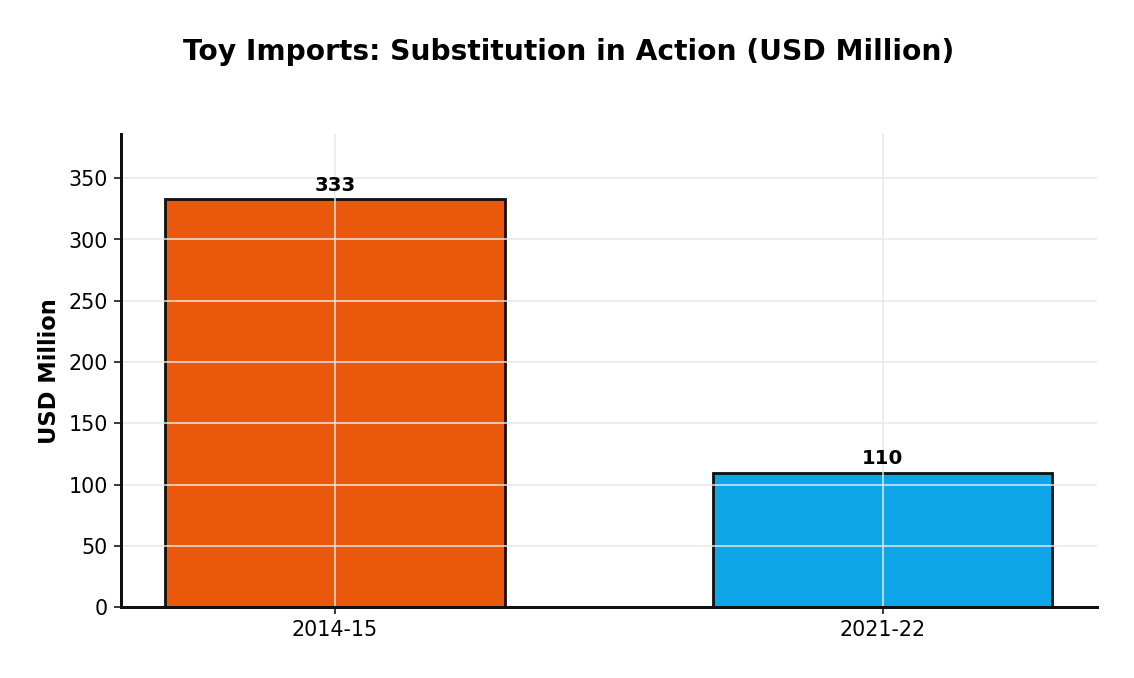

Toys show the same playbook on a smaller canvas. A combination of higher import duties (raised to 70%), Quality Control Orders, and BIS standards drove a dramatic reversal.

Toy imports fell from $332.55 million in 2014-15 to $109.72 million in 2021-22, a 67% reduction. The formula is consistent across both sectors: tariffs plus quality standards plus production incentives reshape an industry.

Where the Smart Money Is Looking

Not every opportunity moves on the same clock. The trade data sorts cleanly into three horizons:

- Immediate (1-2 years): Solar cell manufacturing (policy mandate from June 2026), API intermediates, medical-device components, and food-processing equipment for cashew, pulse, and oilseed.

- Medium-term (2-5 years): Semiconductor ATMP as fabs come online, specialty chemicals, battery components for the EV transition, and technical textiles.

- Long-term (5+ years): Polysilicon production, chip design services that leverage India's IT talent, advanced materials like carbon fiber, and green-hydrogen equipment.

The common thread is that every one of these is anchored in a real, measurable import number, not a forecast or a hope.

Turning Trade Data Into a Decision Engine

The difference between reading these patterns and acting on them is information infrastructure. The raw signals live in public sources, from India's open financial and trade-data landscape on data.gov.in to DGFT bulletins, the TRADESTAT portal, DGCI&S data, and trade databases, but they arrive as fragmented tables, monthly PDFs, and HS-code spreadsheets that are painful to monitor by hand. The founders who move first are usually the ones who can see a category shift the moment it happens.

That is exactly the kind of problem a custom data partner solves. At DatCrazy we turn scattered trade and market data into live dashboards, monitoring tools, and automated pipelines, so an import-substitution thesis becomes something you can track, pressure-test, and act on in real time rather than rediscover a quarter too late. If you are sizing one of these opportunities, the right data system is what turns a promising number into a confident decision.